Life Insurance Death Proceeds Are Quizlet / Capital Dividend Account Tompkins Insurance Services. Life insurance proceeds paid to a named beneficiary are generally free of federal income taxation if taken as a lump sum; The death benefits will be paid to the insured's estate if there are no beneficiaries available. When you're comparing quotes for a $720,000 term life insurance policy, consider raising the number if you can easily afford the premium. Search create log insign up 7 matching questions 1. All types of permanent life insurance policies have a surrender period.

An exception would apply if the benefit payment results from a transfer for value, meaning the life policy is sold to another party prior to the insured's death A death benefit may be a percentage of the. In these cases, the life insurance proceeds are paid to the insured's estate, which consists of all of their assets and debts upon death. Therefore, if you were to. Prior to the introduction of universal life insurance in the early 1980s, the only permanent insurance available to policyowners was whole life insurance, which required a policyowner to pay a fixed, given amount of premium each year, in exchange for having a fixed, given death benefit, and a progression of fixed cash surrender values over time (all.

Life Insurance Flashcards Quizlet from quizlet.com Death benefit is the amount on a life insurance policy, annuity or pension that is payable to the beneficiary when the insured or annuitant passes away. Insurance companies use mortality tables to help protect life expectancy and probability of death for a given group. However, when life insurance is owned by an ilit, the proceeds from the death benefit are not part of the insured's gross estate and thus not subject to state and federal estate taxation. Yearly reductions in face amount If at least one of the designated beneficiaries survives the decedent, the life insurance proceeds pass directly to the beneficiary outside of probate. The free look period for a life insurance policy issued before 1/1/2009 was 10 days. First in line to receive death benefit proceeds the beneficiary of a life insurance policy is the person or entity designated in the policy to receive the death proceeds. Borrower's dependents lender how are level term policies able to provide level premiums?

See topic 403 for more information about interest.

So while the entire death benefit amount remains tax free, any interest earned on it will be taxable. If the borrower is unable. What if both the primary and secondary beneficiary on a policy are deceased or both designations are invalid? Death benefit is the amount on a life insurance policy, annuity or pension that is payable to the beneficiary when the insured or annuitant passes away. There are price breaks at every $250,000 increment, so $750,000 might actually cost you less than $720,000. Borrower's dependents lender how are level term policies able to provide level premiums? In these cases, the life insurance proceeds are paid to the insured's estate, which consists of all of their assets and debts upon death. The life insurance death benefit replaces the financial support you offered to your loved ones if you die. In most, but not all cases, life insurance death benefits are not taxable income. Which of the following statements regarding life insurance is true? Insurance companies use mortality tables to help protect life expectancy and probability of death for a given group. Life insurance death proceeds are generally not taxed as income. A measure of the number of deaths in a given population.

An exception would apply if the benefit payment results from a transfer for value, meaning the life policy is sold to another party prior to the insured's death The death benefits will be paid to the insured's estate if there are no beneficiaries available. The life insurance death benefit replaces the financial support you offered to your loved ones if you die. Brief history of permanent life insurance. In general, beneficiaries receive the death benefit of a life insurance policy income tax free.

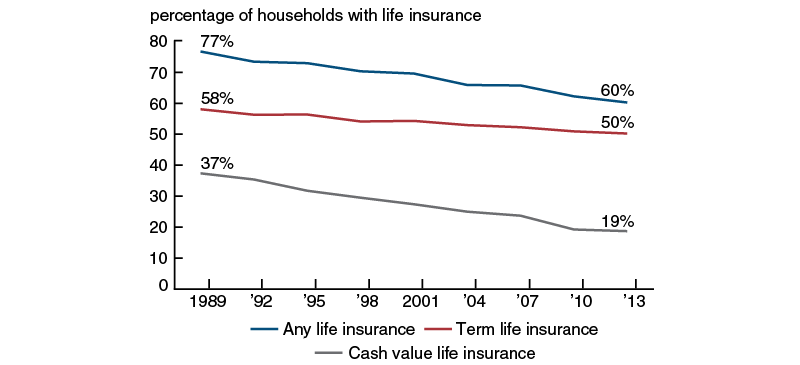

What Explains The Decline In Life Insurance Ownership Federal Reserve Bank Of Chicago from www.chicagofed.org For income replacement, you need a life insurance policy with a $720,000 death benefit. But proceeds from your estate could take up to a year to be distributed and may be subject to tax. An exception would apply if the benefit payment results from a transfer for value, meaning the life policy is sold to another party prior to the insured's death First in line to receive death benefit proceeds the beneficiary of a life insurance policy is the person or entity designated in the policy to receive the death proceeds. A death benefit may be a percentage of the. In most, but not all cases, life insurance death benefits are not taxable income. If an individual designates a charitable organization. Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them.

Search create log insign up 7 matching questions 1.

When an individual designates a charitable organization as the beneficiary of his life insurance policy, the individual can deduct the face value of the policy as a charitable contribution on his income tax return. There is generally no tax applied to the death benefit. The death benefit amount depends on your income and financial situation. The life insurance death benefit replaces the financial support you offered to your loved ones if you die. A collateral assignment of life insurance is a contract that allows the death benefit of a life insurance policy to be used as collateral for a loan. Yearly reductions in face amount If an individual designates a charitable organization. All types of permanent life insurance policies have a surrender period. Prior to the introduction of universal life insurance in the early 1980s, the only permanent insurance available to policyowners was whole life insurance, which required a policyowner to pay a fixed, given amount of premium each year, in exchange for having a fixed, given death benefit, and a progression of fixed cash surrender values over time (all. If at least one of the designated beneficiaries survives the decedent, the life insurance proceeds pass directly to the beneficiary outside of probate. A collateral assignment of life insurance is a conditional assignment appointing a lender as the primary beneficiary of a death benefit to use as collateral for a loan. A death benefit may be a percentage of the. This form of income differs from what you get from a viatical settlement, life settlement or an accelerated benefit rider, because it is coming from the cash value and not the death benefit.

There are few restrictions on who may be named a beneficiary of a life insurance policy. When life insurance is part of an estate a life insurance policy has one or more designated beneficiaries if the decedent completed a beneficiary designation form for the policy before their death. However, it can also be used for equipment loans, structured settlement buyouts, and other loans. The life insurance death benefit replaces the financial support you offered to your loved ones if you die. Search create log insign up 7 matching questions 1.

Kentucky Life Insurance State Exam Practice Flashcards Quizlet from up.quizlet.com However, this is not always. Upon your death, your family can be assured that the amount you've chosen—perhaps hundreds of thousands of dollars, maybe even millions—will be there almost immediately. Death benefit is the amount on a life insurance policy, annuity or pension that is payable to the beneficiary when the insured or annuitant passes away. Life insurance proceeds that are received by a beneficiary aren't taxed and are available almost immediately after death in a lump sum or annuity payout. Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them. For income replacement, you need a life insurance policy with a $720,000 death benefit. When life insurance is part of an estate a life insurance policy has one or more designated beneficiaries if the decedent completed a beneficiary designation form for the policy before their death. This form of income differs from what you get from a viatical settlement, life settlement or an accelerated benefit rider, because it is coming from the cash value and not the death benefit.

Interest paid by an insurance company on a death benefit, however, is taxable as ordinary income to the beneficiary.

However, it can also be used for equipment loans, structured settlement buyouts, and other loans. The person entitled to the proceeds of a life insurance policy upon the insured's death. Life insurance proceeds paid to a named beneficiary are generally free of federal income taxation if taken as a lump sum; First in line to receive death benefit proceeds the beneficiary of a life insurance policy is the person or entity designated in the policy to receive the death proceeds. The policyowner may select a settlement option at the time of the application and may change the option at anytime during the life of the insured. Life insurance death proceeds are generally not taxed as income. The death benefit amount depends on your income and financial situation. Therefore, if you were to. If at least one of the designated beneficiaries survives the decedent, the life insurance proceeds pass directly to the beneficiary outside of probate. In most, but not all cases, life insurance death benefits are not taxable income. Life insurance proceeds that are received by a beneficiary aren't taxed and are available almost immediately after death in a lump sum or annuity payout. A death benefit may be a percentage of the. The life insurance death benefit replaces the financial support you offered to your loved ones if you die.

0 Comments:

Posting Komentar